Retirement Income and Spending

(00:00):

This is a two part series, Dollars and Cents, where today we’re going to be talking about the dollars part of retirement income and spending. So that is definitely a hot topic which is why we’re talking about that today. It’s a huge question for anyone starting the process of thinking about retirement, shifting from accumulation to actually drawing income off of assets and figuring out, well, do I have enough to retire?

It’s also a great topic and something worthy of deep thought for people who are already retired because a lot of people just don’t know what’s okay – “how much can I spend?” You want to be able to utilize it to enjoy your retirement and really make the most of your life. .

But before we get started, I should introduce myself.

(01:01):

My name is Sheena Hanson, financial advisor with Uncommon Cents Investing. I truly do love the topic of financial planning to compliment investing. Certainly we talk a lot about investing, and that’s kind of why I asked Amy to join us as well, to talk about the psychological aspect of this retirement income topic. So again, just to introduce Amy, this is Amy Ginsburg, and this is the second time we’re partnering. I’m looking forward to everything she has to say about the psychological aspect of retirement and drawing income. Amy is a professional certified coach focusing on retirement transition, and so she really is great at supporting people in their journey through that.

(01:55):

Just a couple more things. Anything I say today is not tax advice, it’s not legal advice. I live in a world full of regulations, so I want to make sure to say that – anything that I say today is not really advice, it’s just education. I really want everyone to be aware of what’s possible, and with everything having to do with retirement income. If you do want advice regarding this topic and your situation, certainly reach out to me at a later date and we can kind of dive deeper. Today we will be covering two main things.

- How much can I withdraw from my investment in retirement? It really is a huge gray area. It is not black and white and it’s unique to you. So what’s that number? What am I okay to withdraw from my retirement to accomplish what I want

- How do I start drawing income from my investments, and questions surrounding what accounts to draw off first? Do I withhold taxes? Most retirees I find in practice, through having many, many conversations with people about retirement, share some common ideals regarding funding. The first one is to maximize withdrawals, especially early in retirement. People who are in their sixties, they feel good, they’re healthy, they’re very mobile, they want to do everything they can early in retirement. Number two, eliminate the possibility of running out of money. Certainly we want our assets to last our lifetime and potentially leave a legacy to our beneficiaries so we don’t want to run out.

(03:58):

Also, avoiding undesired changes to their income stream – that lifestyle continuity. If people are used to going out to dinner every Friday and Saturday night or spending lavishly on Christmas gifts for the grandkids during their working years, they don’t want to stop that during retirement. So we really want to just keep our lifestyle for the rest of our lives, and of course, maintaining purchasing power. We’re in a world now where inflation is pretty high and cost of goods do go up over time, and so we want our income to reflect and support that. But before we jump ahead into retirement spending, I want to break it down. I think we need to look at income as a whole and really what are all the components of retirement income, before we just focus on drawing off of our investible assets.

Sources of Retirement Income

Gradual Transition into Retirement vs Full Retirement

(04:57):

For typical sources of retirement income, I’ve got two scenarios I wanted to show you, and they really are representative of what I mostly see.

The first example is someone who is phasing into retirement, which is more and more common. Instead of doing the 180 degrees, working full-time – 40, 50 hours a week – and then just stopping, it is more of a gradual transition – maybe early retirement into something else, having part-time income in retirement. And so this person might have a little bit of pension income, some social security coming in, the income from savings and investments, but then also their post-retirement work earnings from their second gig or that part-time income.

Then there is someone who is fully retired. You may have heard of the term, the three-legged stool? We have a lot of people who have pension income still, although that will gradually become a thing of the past because as we all know, pensions are going away. So if someone’s fully retired, and they want to have a retirement income of a hundred thousand dollars, maybe $37,000 of that comes from social security, $26,000 from assets and then maybe $34,000 from pension. That’s very representative of what I see.

(06:39):

So things you might want to ask yourself and really dive deeper about this topic of income for you is, where do all parts of my income come from? For someone who’s retired, that’s probably fairly easy to come up with. You can take a look at your bank statements. You’re well aware of what’s coming in from social security, what’s coming in from a possible pension, and what deposits might be made from other sources like withdraws from your IRA, accounts or withdraws from 401k.

It might be more time consuming or a little bit more of a project for someone who’s not yet retired and also kind of thinking about what the future sources of income might be. Another thing to think about here is how much income do we want on a monthly or annual basis?

How Much Do You Want to Spend in Retirement?

(07:36):

I emphasize the word want because so often I hear people expressing income in retirement as, “oh, how much do I need?” “This is how much I think I am going to need to spend on a monthly basis,” but I really like to use the word want because it’s a little bit more glass half full approach, a little bit more abundance mentality. What do I want that to look like versus scarcity, oh, this is how much I need. And so really it’s just thinking about what’s possible. Also, be realistic with yourself. Know your spending habits. Really dive deep in your credit card statements or bank statements to really know what your spending habits are. If I ask someone, what do you think you spend, most times people underestimate what is actually going out of their pockets.

Two Other Considerations:

1. Emergency Fund in Retirement

(08:35):

Another thing to think about, do I have a reasonable base of liquid cash? How much cash is in the bank? Emergency funds, sometimes even an irrational amount of money in the bank if that makes you feel comfortable and sleep at night, that’s also something to think about when really thinking about retirement and drawing income as a whole.

2. Return on Investments During Retirement

Am I funding my future income in a manner that can still grow? I emphasize that because another thing that we talk about a lot while easing into retirement is, well, maybe my investments need to be become more conservative because it’s no longer long-term money. We tend to disagree with that thought process to some extent, and I’ll kind of show you just going back the Typical Sources of Income in Retirement slide in the section above. When you think about the pie chart, the majority of retiree income is fixed income. If you’re living off pension, if you’re living off of social security and all of a sudden two thirds of your income are coming from fixed sources that are for the most part safe, they might also get that cost of living adjustment for inflation. Really, it is very important to keep the assets in growth mode – from an income perspective, you don’t want to be too conservative. It’s very important to keep assets growing in retirement.

Example: Retirement Income and Expense Analysis

(10:05):

Alright, so let’s keep going here. Here’s an example – Judy and Jim. This is an example that I thought of just off the top of my head, so it’s a fictitious example, but very representative of what I see in our clientele and their retirement situation. Judy is 64. Jim is 66. Judy is a retired teacher and has a WRS pension and has filed for social security. Jim is retired from a local manufacturing company, but works part-time because he likes to keep busy and has decided to delay social security until he turns 67. They own one duplex where they earn monthly income since one side is being rented, and Judy’s aging mother is living independently in the other half rent free, and they are debt free.

(11:18):

Assets include cash in the bank of $60,000, and 401ks, 403bs and IRAs and retirement savings of $750,000. So they’ve done a great job saving! For real estate, their duplex is valued at $350,000 and their primary residence, their home, is valued at $350,000. So let’s revisit their income sources one more time.

Judy has the WRS pension that she’s receiving for $1,500 a month and social security for $2000 a month. Part-time income from Jim for $1500 a month and then their rental income for $1000. A total income is currently $6,000 per month to support their lifestyle. Through this process, they did their income analysis and now they know where they stand. The second part of their retirement income analysis is their expenses. So going through that, Jim and Judy have figured out that they want to have a $7,000 per month retirement income, so they’re about a thousand dollars short on where they want to be.

(12:43):

So typical questions, once people arrive here and they know what the shortfall is, are “where should we draw that from?” “Which accounts should it come from? Our IRAs, our pre-tax accounts?” “Do we draw from our Roth?” “Where should we go from here?” They are more the “how do we do that questions?”

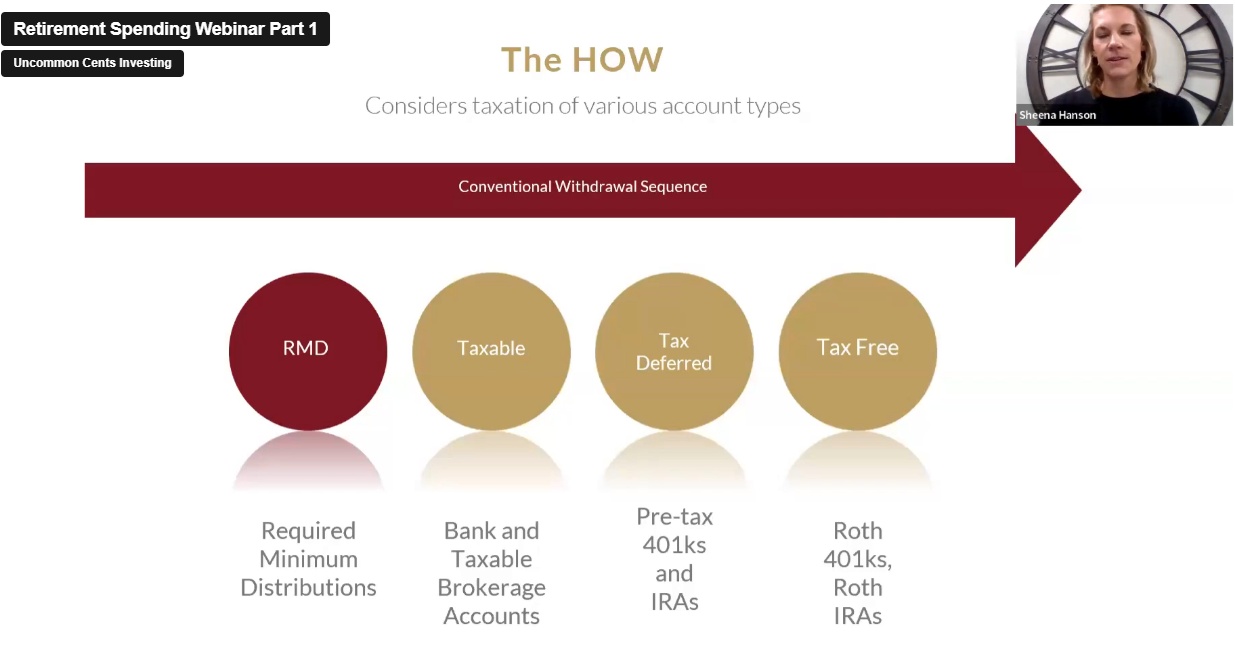

Then the other questions that come up are the… “well, is that okay?” “Am I going to be drawing too much money off of my assets?” “Am I putting myself at risk in any way?” They are recognizing that they are no longer just saving inside of our retirement vehicles, but that they’re also going to be withdrawing and taking money out. So that’s the how logistically, how should we be drawing retirement income from our investment? At this point, we really need to think about taxes. So, taxation is strongly evaluated at this stage. Most people see the conventional withdrawal sequence as starting with required minimum distributions.

Typical Retirement Withdrawal Sequence

1. Required Minimum Distributions

(13:55):

For those of you who don’t know, RMDs are set by the IRS to start at age 73. So people do need to plan to start drawing off of their pre-tax investments at age 73. This really doesn’t apply to Jim and Judy. They are not at required minimum distribution age yet, so that’s not an issue for them. Next on the table would be taxable investments.

2. Taxable Investments

So what are taxable investments? Typically that includes non-retirement brokerage accounts – cash in the bank primarily. Those are the first places to think about drawing retirement income from, and I’m going to dive into the taxation of that here in a minute, but just know that those accounts really are our first to go. Second on the block really is tax deferred investments. So this includes your pre-tax, 401ks and IRAs. Money and retirement accounts that have not yet been taxed.

3. Tax-free Accounts

(14:50):

And then third and finally is the tax-free account, which includes Roth money – Roth IRAs and Roth 401ks. That is the conventional traditional sequence from a tax perspective of where you should draw from first. This really is good rule of thumb advice for people who have a pretty set retirement income. It’s steady and it really doesn’t fluctuate.

For people who may have fluctuating income where some years are high income years and other years are lower income years, I would say it would be worth talking with us or a tax advisor to really think more efficiently about where to withdraw from if you have some severely fluctuating income. Just to revisit the tax tables here, there’s a couple of areas that right now with today’s tax code are worthy of attention because there are opportunities.

There’s kind of two sides here on the chart.

(16:00):

The red that indicates the income tax rate, is really just the ordinary income tax tables. And so we can see on a marginal basis people are taxed to start with 10% and then it increases from there up to 12%. And then, for someone who’s married filing jointly above $89,450 taxable income, it jumps up to 22% tax bracket.

So on the ordinary income rate, sometimes we talk about Roth conversions between the 12% bracket and the 22% bracket. And then on the right hand side of the chart, when we’re thinking about long-term capital gains and qualified dividends, people who make under a certain amount of income threshold can potentially be taxed at 0%. And so I emphasize that a little bit because going back to our previous slide, why do we recommend drawing off of taxable accounts first, which typically includes brokerage accounts, bank accounts? Because a lot of times if you’re drawing off of a bank account or even a non-retirement brokerage accounts, depending on what assets are sold to free up that income, you could potentially have a tax-free withdraw by drawing off of those first. So it’s really the how to draw off of and where to withdraw – it’s all about taxation.

Strategies and Research

(17:41):

Okay, so let’s get into strategies and research. Before today there was some really analytical white papers and information that I combed over but I wanted to keep everything really high level today for you. “How much” is really what I wanted to spend the most time on today. We love the word safe withdrawal rates. If you’ve had a conversation with John or I, or if you’ve read about how much can you draw off of your retirement accounts, the word “safe” crops up a lot, as in “how much can I safely withdraw from my investments?” Which really points to “how much can I safely withdraw from my investments without outliving my savings?”

4 Withdrawal Strategies

These are four different common and effective withdrawal strategies. I’m going to get into those a little bit deeper, but just an overview.

- Systematic withdrawals: taking a fixed dollar amount and adjusting that a little bit each year. It’s a rather simple calculation.

- Dynamic withdraw strategy: This one also starts with a fixed withdraw rate, but it’s dynamic in the sense that it accounts for the stock market and the fluctuations on the upside and the downsides.

- Income only: I don’t see this as much from people coming up in conversation, but it is something that people still do, only drawing income off of their investments, which would include dividends and interest that comes into the account. The main purpose of it is to not touch the principle of your investments and only draw off that income.

- Only taking out required minimum distributions: This does start naturally at age 73 for people who have IRA accounts and 401ks, but you actually can take the required minimum distribution approach even earlier in life if you choose to because it is based off of life expectancy and IRS life expectancy tables. So you really could calculate a required minimum distribution amount even on earlier ages prior to age 73.

The 4% Rule

(20:09):

So what is the 4% rule? Let’s define that. The traditional 4% rule is a retirement planning rule of thumb that dictates how retirees withdraw. It’s 4% of their retirement funds in the first year removing that dollar amount from their account, and then after that we adjust it for inflation every single year. And so the most widely used definition of a safe withdrawal rate is this definition adjusting for inflation.

So let’s take a look at this from a dollar perspective, standard rule of thumb with 4% adjusted for inflation. Again, kind of going back to the fact that I like round numbers, let’s think about someone with a million dollar portfolio. They have a million dollar IRA and they’re going to do 4% withdrawal, adjusted for inflation and the assumed rate of inflation here is 3%. So in year one, the retiree would withdraw $40,000, that’s 4% of a million dollar portfolio, and then in year two, they would take that starting withdraw amount, $40,000, adjust it for that year’s rate of inflation, again 3% in this example. So year two would have a withdraw amount of $41,200. Year three, again, you just adjust that withdraw amount for inflation. And so adjusting that again would take it up to $42,436.

(22:09):

The person who came up with this rule, just to share a little backstory here, is Bill Benin. He’s known as the father of the 4% rule. How he arrived at this is that he took someone with an asset allocation portfolio of 50% stock, 50% bonds, and did all these trial and error runs through all kinds of different market scenarios. He took a 50 year period from 1926 to 1976 – really focusing heavily on the downside risk of the 1930s and 1970s. What he found through all of this analysis is that a 4% annual withdrawal never, in any circumstance, exhausted a retirement portfolio in fewer than 33 years. A lot of people have an expected retirement timeframe of about 30 years, although certainly some people have retirement time horizons that are a lot less, and some people have those that are a lot more. It’s really not my favorite rule, if I’m being honest. What I don’t like about it is that it does not take into consideration market volatility. It doesn’t guarantee that your purchasing power will remain constant.

(23:44):

Sometimes the actual cost of goods rise a lot faster than the actual stated inflation rate by the government. As I mentioned just now, you may live longer than 30 years. So what if you retire at 60 and you live to be a hundred? That’s a 40 year retirement. And with medical technology advancing quickly, people really are living longer. Also, the success depends on the allocation of the portfolio. So Bill’s research was done using a 50/50 allocation to stocks and bonds. Some people have much more conservative allocations, and so if that’s true, 4% may not work. It also doesn’t take into consideration changes in economic or personal condition.

(24:37):

Really, the best thing to know, and I think the biggest takeaway here is that it’s best used as a starting point. Four percent is a good starting point. I like this example. The bell curve gives a really good visual.

Are you someone who ideally in your retirement wants to spend all the money that you can? You want to bounce the last check on your deathbed? That’s not most people, but there are people who believe that. And then there’s other people who are on the other end of the bell curve. They want to maximize legacy, and so they don’t want to draw as much income off of their portfolio. They want to pass it on to their kids or to nonprofit organizations. And they have other goals besides just using it as income.

(25:27):

But most people do fall in the middle of that bell curve. They save their retirement money for income they need to be drawing for themselves, but then also they may have other objectives as well. So similar to betting all of your chips at the poker table, you’re probably going to want to fall in the middle of the bell curve (not too aggressive or conservative), like most people. But that also is worthy of reflection and talking with your spouse, “really what are our goals and what are we trying to achieve with our retirement income?” Figure out what withdraw approach is best for you.

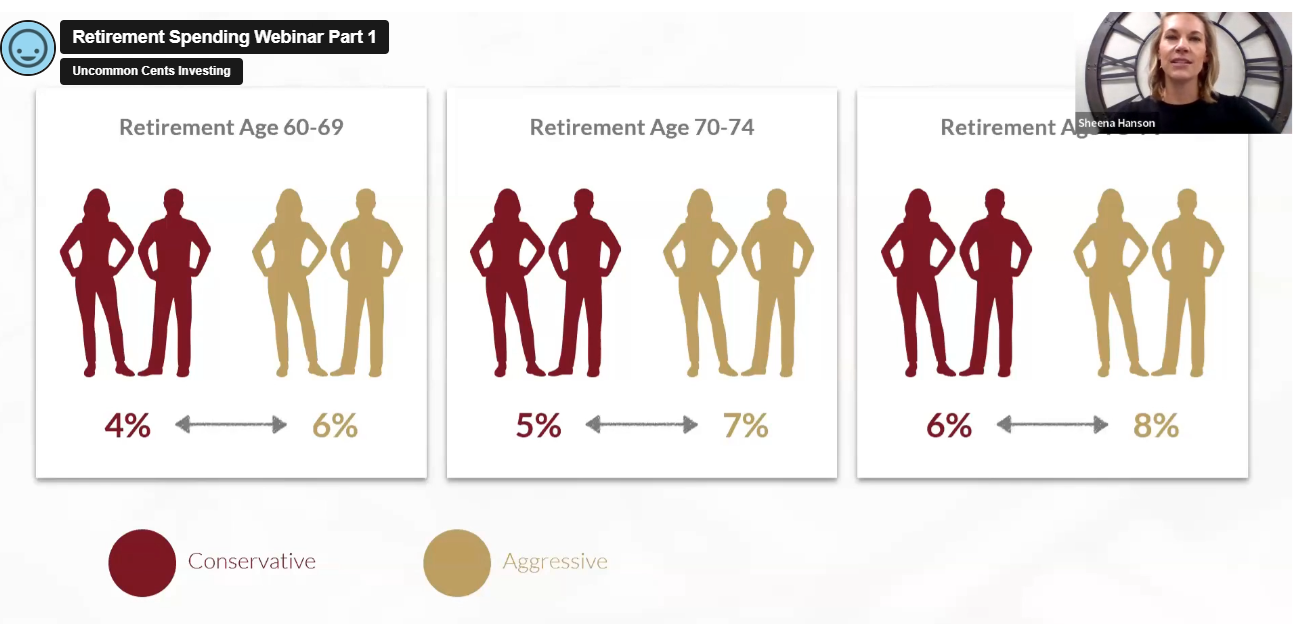

So this might be my favorite slide of the entire presentation because it really shows what I believe to be, and what we believe at Uncommon Sense Investing to be, safe withdrawal rates. And the biggest things to think about here is that age and longevity are really probably the top things to think about when thinking about a starting withdrawal rate. Also, how much of your income is dependent on what you’re drawing off of your personal investments?

(26:35):

People who plan to work longer in retirement or have some significant pension income might be able to use higher withdrawal rates. And so these are starting ranges for people who are 60 to about 69 years old, 4% to 6% depending on the objectives, how your portfolio is allocated, what your goals are is the range where you need to be as a starting point, ages 70 to 74, you really can take more money out and I’m going to get to the math on that in the next slide, 5% to 7%. People who are later on in retirement, you are able to take more because it kind of goes back to that longevity. How long are you expected to live?

(27:27):

Let’s look at simple math, keeping it simple. The original research was based on a 30 year expected retirement. So let’s think about worst case scenario. What if, the odds on this are not likely, I don’t believe this has ever happened, but what if, during that 30 years you received a 0% rate of return on your investment? So we can take one hundred percent of our portfolio’s value divided by 30 years. That gives you 3.33%. So you could draw 3.3% off of your portfolio over 30 years with a 0% rate of return, and then at the end, in turn have $0 left.

(28:15):

So looking at the mortality tables for a 70-year-old woman – a 70-year-old woman is expected to live about 17 years. So 100% of a portfolio divided by 17 years equals 5.88%. So again, assuming a 0% rate of return, one could draw, given 70-year-old woman’s example, almost 6% of their portfolio. If we’re only considering worst case scenario life expectancy, that’s kind of where those ranges come from if you’re really kind of wondering what the thinking and what the thought process is behind that.

So here I’m going to pause for a minute because there’s been a lot of information. Sometimes when it’s information overload, analysis paralysis is a real thing, but we’re trying to take this one step at a time and this first step for you is just watching this webinar, getting the information and then subsequently taking steps to drill down on figuring out your retirement income situation, hopefully including us on that conversation as well.

Determining Your Optimal Rate of Withdrawal During Retirement

(29:36):

What factors should be considered in order to determine your personal most optimal rate of withdrawal?

- Allocation of your portfolio: How heavily are you allocated to stocks, bonds, and cash? Certainly expected rates of return will vary, and for someone who is more aggressive – we do have people who are retired and they have portfolios that are a hundred percent in the stock market – expected rates of return are typically eight to 10% over the long-term. And so you might be able to account for potential higher withdraws because of that more aggressive stance.

- What age are you making your withdrawals: that is going to also strongly dedicate what a safe withdraw rate is. If you’re 60, you are most likely going to think more about sticking in that four to 5% starting withdrawal rate. If you’re someone who’s worked, who’s delayed retirement, delayed drawing off of your investments and you’re 70, you’re going to be able to enjoy more, feel comfortable taking more money out spending.

- How is the stock market expected to perform: As we know stock markets go in cycles. How attractive is the stock market in the moment? Are we expecting it to be a very robust future? Is the stock market cheap, that can be good for retirees, or maybe it’s the other side? Is the market going through a more muted period? Are expected rates of return going to be subpar because if that’s the case, withdraws might need to be a little bit more conservative to start with. And I think that’s potentially the market that we’re in right now for early retirees.

- Longevity: how long are you and your spouse expected to live?

- Do you want to leave money behind: How important is that legacy for you?

- And then of course it’s what I call the can you sleep at night? What is your overall comfort level with the rate at what you’re drawing off your portfolio: I can tell people all day long after looking at a situation, assessing everything and then arriving at a number or maybe a percentage, okay, you can draw 5% off your retirement, you can draw 6% off of your retirement. And if you’re not comfortable with it, that might not be the number that works for you. You might be comfortable 3% or 4%. And so it really does come back to what are you comfortable with?

We talked about various approaches to sign off of income, mainly the 4% rule factored by inflation annually, which is the traditional approach. So now I’m going to talk about the Uncommon Cents approach and how we think about the 4% rule around here.

The Uncommon Cents Approach to Retirement Income Planning

(32:54):

Let’s circle back to the big limitations of the 4% rule. The first one being it does not account for market volatility, and then the second one being, it does not account for portfolio allocation, or how aggressive are you with your investments. So the way that we like to account for the 4% rule to try to lessen some of the limitations of the traditional 4% rule is this way, and it’s shown on the screen here.

What we like to do is take the annual withdraw, which would more or less be 4% of the prior year account balance. Let’s go back to our million dollar example to see how different that might look from the more static 4% approach for million dollar initial portfolio value. Year one, we start with a $40,000 withdraw. But if we’re taking the prior year account balance and how the market has performed throughout that year, if it was positive, if it was negative, that calculation is going to factor in how the market performed.

(34:05):

So year two, let’s hypothetically say it was up 10%. Well that means your income, how much you’re able to take out of your investments, increases. That’s a good thing. Over time using this approach, we know that most markets are positive and so over time your income will be able to grow along with that. Year three, if it’s a negative market times are not so rosy and there’s a negative 5% performance rate on your investments, well then your income is going to go down to $38,000 roughly. And year four, let’s just say the market’s back up again, it’s earned some of that back and now you’re up 6%. You’re kind of back to where your income started at $40,000, in this case just a little bit more. And so what I love about this approach is that it really factors in the fluctuation of the market and it also follows people’s natural tendency if you want to spend more in good times.

Advantages and Disadvantages of this Approach

(35:03):

I do see that behaviorally people are more willing to draw off of their investments – spend more money, go on vacations – when times are good, and also to tighten the belt when times are not so good. That’s just human nature. You’ve probably done that throughout your entire lives and that certainly is not going to change in retirement. Also, like I said, it really allows your income to grow with your portfolio performance. I think that’s always a good thing for retirees, to kind of have that growth of income along the way, even over and above inflation. Also, it hedges against that poor market performance, especially if it’s prolonged. I mean that really is the big danger for people is if there’s a prolonged period where the market just doesn’t perform how we want it to.

The disadvantages, of course it’s still a “rule of thumb.” It does not account for your specific situation, and your income will fluctuate. There’s some people that they don’t want their income to fluctuate, so they really would prefer a more set number, something that’s more consistent along with their social security and, potentially, their pension. So the big thing here is that you are unique, and this is so important because the last thing that I would want any of our clients or anyone to do for that matter is just to take the 4% rule as a rule of thumb because in many ways you’re just limiting your potential retirement income. And again, I’m all about a retirement that is full of abundance and enjoyment and that is really impacted heavily by your income level.

Back to Judy and Jim

So let’s get back to Judy and Jim. Remember they would like to have an extra thousand dollars per month, but how should they withdraw it? Will they be okay? Let’s review their assets one more time. Cash in the bank of $60,000, and retirement assets of $750,000. And then of course their real estate investments that are each valued at a $350,000 market value.

(37:24):

Real estate is not liquid. I really don’t consider real estate when I think about calculating retirement income and where to draw off of. I think of it as a completely separate entity, although there are other ways to factor in real estate with drawing income. And so just know that if you are a real estate investor, the total assets outside of their real estate is $810,000, and if we take that starting 4% rule, they are able to have an income of $32,400 per year, or an extra $2,700 per month. So again, kind of going back to what is the starting percent, if Jim and Judy were in a different age bracket, different situation, that might be 5%, that might be 6%, it might be 2%. So it really depends on the situation as to how to start.

Judy and Jim can easily take out an extra thousand dollars a month. They’re very happy to know that in fact they could take out more. They could take out $2,700 if they chose to. We know they have $60,000 in the bank, so that’s where I would advise them to start with first, start drawing off of money in the bank and then we’ll start tackling their retirement savings, kind of going down the rules of taxation.

But they might not be comfortable with that. They might tell me, “Hey Sheena, I know you said I should start drawing income off of those assets in the bank, but we don’t want to do that. We really like to have $60,000 as an emergency fund and that’s our safety zone, that’s our comfort level.” So then I would say, “fine, Judy and Jim, no problem. Let’s then take it from your retirement accounts. We’ll take it from your IRAs. We’ll set up distribution from your 401k and we’ll do it that way.”

(39:27):

So Judy and Jim, they’re now armed with the power of knowing their income sources, knowing their spending, knowing how much they can draw off of their investment accounts in retirement. But how else might this information be empowering?

Remember, Jim is working part-time. He is earning $1,500 a month on the job, kind of phasing into full retirement. And so now that they know that they actually can safely draw off $2,700 from their investments, they feel a much larger sense of freedom knowing that if he stopped working, they could replace his income and feel pretty good about that. So now this is where we see that information is power. They have many more choices at their disposal.

Other common situations that might be counterintuitive that I see a lot,

- People who draw higher amounts off of their personal savings and investments to retire earlier, there’s often a lot of massaging and people are in limbo between age 60 and 65 as they’re easing their way towards Medicare age, easing their way towards turning on social security.

- Sometimes you can justify a higher withdrawal rate off of personal investments to either pay down debt and to improve cash flow. Just account for turning on income from your portfolio and then potentially turning that income off once social security starts.

- Keeping debt and retirement due to lower interest rates locked in if cashflow allows for it.

So these are just some examples where that income rate that you set to start with, it might change over time depending on how things go.

3 Phase of Retirement

(41:27):

These are the common three phases of retirement. I just want to mention briefly, the go-go years, the slow-go years and the no-go years. You may have heard that before and it is true, our bodies change in retirement as we get older. Certainly we’re not as energetic as we are when we’re 60 or 65. So many people want to do a lot in that first decade of retirement, but as that process moves along with the aging, things start to slow down. And then finally, you might not be traveling as much anymore or enjoying the entertainment aspects of your life that you had previously. And so this really does come to fruition for most people.

Summary

(42:22):

Let’s go back to the key takeaways from today. Drawing income in retirement, it really is anything but black and white. I’m not a fan of rules of thumb, but I think they can work as a starting point. Four percent does not optimize for your specific situation, it doesn’t optimize for most people. And so it is worth taking a deeper dive into what you’re trying to accomplish and all of the variables of your situation. It’s really best to start with analyzing all of your income sources. Where are all of your income sources coming from as it relates to spending? Think about what you want your retirement income to be. If you have a million dollar portfolio and you only need a certain amount to live off of, think about what you might be able to do with that extra income. How can I use the ability to have more income in retirement over and above what I need to really enjoy myself and maximize what I can out of life? What are your goals for your money? Have that conversation either internally with yourself or externally with others and your spouse. What are our goals? What are we trying to accomplish?

(43:43):

And so really ultimately we believe that a dynamic 4% withdrawal strategy can be more effective than 4% plus inflation. And again, I say 4% here, but that might not be the right starting point for you. A more appropriate starting point if we go back to the bell curve, might be more than that, or it might be less than that. And it really is something that evolves over time. It’s not necessarily “let’s set it at 4% and then let’s just continue on for the rest of our lives.” I want to be able to help you maximize your income and set up a strategy that’s right for you. And then lastly, if you start withdrawing later in life, – I think that’s probably been clear here, working later, starting withdraws later – or if you have significant pension income, your withdraw percentage can still be higher and effectively and be safe.

(44:44):

Alright, before I get into some other conclusions, I’m just going to address a question here from the question and answer section, the question says, “if the last time you determined your annual spending was five or more years ago, are spending levels still okay, or should you redo your spending levels for current years?” Alright, spending analysis, okay, I think we’re all aware that probably five years ago things just simply cost less. Going to the grocery store, going shopping and doing projects around the house, things cost more. And so absolutely, I think if you have not done a spending analysis recently and you’re entering into that income phase in retirement where you really need to have a closer eye on your spending, things have changed. Redoing that spending analysis is worthy of doing. Five years ago with inflation and how things have changed, cost of living is up and that has to be recognized.

(45:48):

A couple more final thoughts before hopefully I can get into more questions. Current and soon to be retirees who have consistently practiced living within their means and saving, often are in a good place financially. And I feel really good in saying this, that’s most people I see, most people that we work with, are people who we are in the Midwest. We live in Wisconsin, they’ve worked hard, they’ve practiced living within their means. And so that’s how they’re used to living. Once you get into retirement, you’re spending habits just are not going to change. And so that’s great. In fact, that is a notch in the belt for greater retirement security. And so I do find, with my practice and what I see regularly, is that as people phase into retirement, they might be 55 and then they know, okay, I’ve got to stick it out for another five years, and then they get to 60 and then they’re really chomping at the bit, “okay, I need to figure out this retirement thing” people start to figure out what I call “the levers.” “What levers can I pull to make this happen?” There are a lot of levers:

- Do I take out a chunk of my investments or money in the bank and pay down my debt to kind of free up my personal cashflow a little bit better?

- Do I start saving more aggressively in my 401k?

- Do I think about transitioning into a second part-time job or retire from what I’m doing into something completely different where I have more time and control back, but yet I still have some income in retirement before I’m fully retired?

And one thing I want to emphasize is not lever is the stock market. Some people come in here, the first thing they have to say is, oh man, I wish I could retire, but the stock market, it’s just really not doing what it needs to do for me. The stock market is not a lever.

(48:05):

There’s a lot more in your control that you can do to get you to that retirement place outside of just simply depending on performance of the stock market. And then of course, here I have to mention it, those of you who have saved more than you’ve ever dreamt possible, a lot of times you have my permission to spend it. Think about ways to enjoy it for you and your retirement or in some cases gifting. There’s a lot of things that you can do with your money outside of just spending and being frivolous. But a lot of our retirees have just done really wonderful things financially. And so it’s worthy to pause and think what can I do with this money? How can I make my life greater? How can I really maximize what retirement is for me?

(49:05):

And so with that, everyone, thank you for attending. That really is today’s content. I hope you found it to be very helpful. I will stick around if anyone else has questions that you might want to type into the question and answer chat to just really address any kind of final thoughts and concerns. One thing I will say is that this content is something that you might want to come back to if you’re not quite at retirement or even if you’re in retirement and you want to think about how you could maybe make more out of your retirement income.